The following is an excerpt from a recent Market Comment featured on The Felder Report Premium.

“Earnings don’t move the overall market; it’s the Federal Reserve Board… focus on the central banks and focus on the movement of liquidity… most people in the market are looking for earnings and conventional measures. It’s liquidity that moves markets.” –Stan Druckenmiller

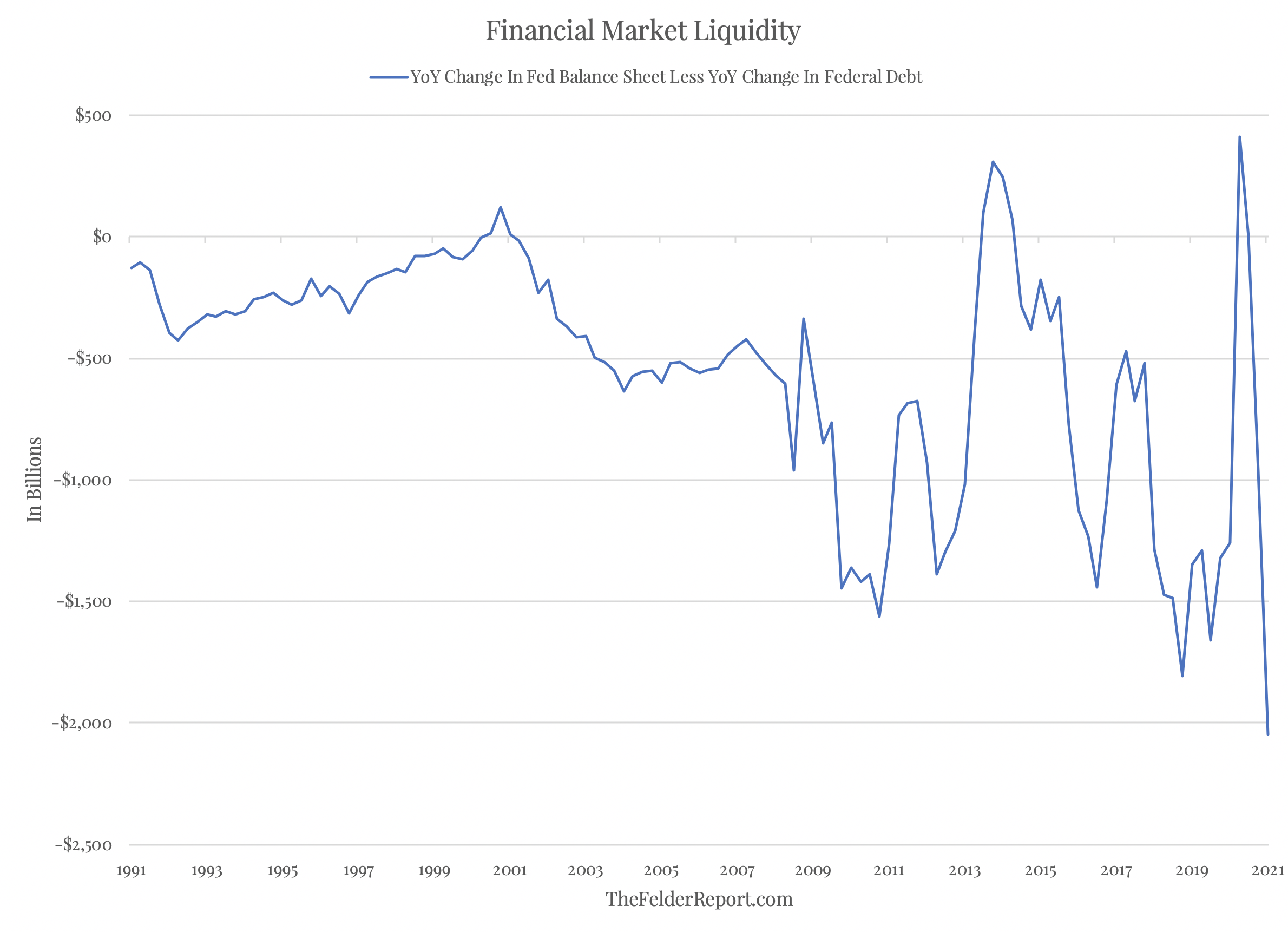

If there’s any lesson investors have learned over the past decade, it’s this one. ‘When the Fed is making the money printer go “brrr!” it’s time to buy stocks!’ But there is more to it than the simplified version of “liquidity” most traders have adopted. It is not only about how much money the central bank is printing; it’s also about how much debt the federal government is issuing. And it’s the difference that really matters most to the markets. In his recent interview with the Economic Club of New York, Druckenmiller tried to clear up this misconception:

If there’s any lesson investors have learned over the past decade, it’s this one. ‘When the Fed is making the money printer go “brrr!” it’s time to buy stocks!’ But there is more to it than the simplified version of “liquidity” most traders have adopted. It is not only about how much money the central bank is printing; it’s also about how much debt the federal government is issuing. And it’s the difference that really matters most to the markets. In his recent interview with the Economic Club of New York, Druckenmiller tried to clear up this misconception:

The consensus out there seems to be, “don’t worry, the Fed has your back.” …There’s only one problem with that is our analysis says it’s not true… I stated earlier that the Fed has increased their balance sheet from four trillion to eight trillion. While they’ve done that, the Treasury Department, I’d say the budget deficit estimate for this year has gone from maybe a trillion a year ago to three-and-a-half trillion… So in March and April alone, the Fed net of Treasury issuance, to pay for the new spending, created a trillion in QE more than Treasury issuance. So it’s the biggest liquidity injection relative to history I’ve ever seen… The problem is as you look forward, because the Treasury deficits are not only still gonna be there, they’re just rolling out aggressively now the financing of them, the Fed front ran this with their actions of a month or two ago and so what the Fed bought was a trillion more than treasury issued. What’s going to happen now is Treasury issuance has caught up with the Fed and if they stick to the schedule they’ve outlined the net difference between those two actually goes to zero in May and net borrowing by Treasury relative to Fed purchases in June very minor, pretty much flat through September. And then liquidity shrinks as far as the eye can see as the Treasury borrowing crowds out not only the private economy but even overwhelms Fed purchases… That leads me to believe… the risk for reward for equities is maybe as bad as I’ve seen it in my career here.

It’s hard to be more plain-spoken than that even if it is a bit meandering. Contrary to popular belief, liquidity is not the tailwind for risk assets most traders believe it to be. In fact, it will soon be just the opposite. Net positive liquidity has already evaporated and will soon become a net negative because, even as the Fed prints record amounts of money, it will be overwhelmed by the money being sucked out of the markets by the rapidly growing needs of the Treasury.