FRED recently updated the data I’ve been using for my fundamental and sentiment measures from Q1 to Q2 of this year so I thought it would be a good time to post an update to my market-timing model (see “Seeing The Forest For The Trees“).

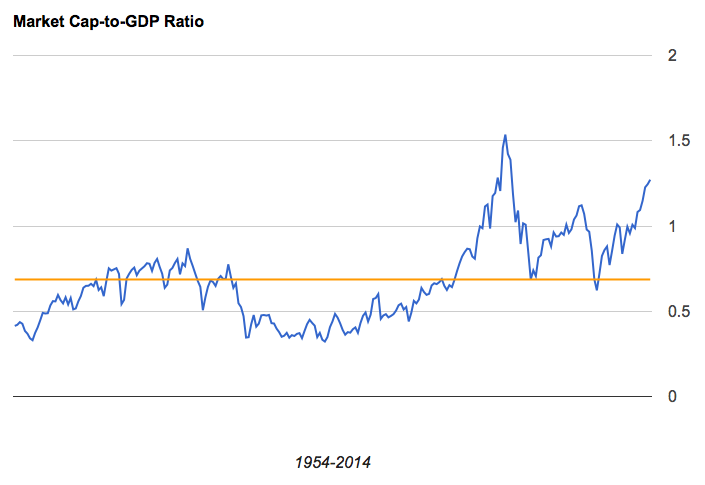

First, there is the fundamental component for which I use Buffett’s favorite valuation yardstick: total market cap-to-GDP:

Over the past 60 years there has only been one time where stocks were more highly valued and that was during the height of the internet bubble.

This component is nearly 90% negatively correlated to future 10-year returns for stocks (higher readings are correlated with lower returns and vice versa). Right now it’s forecasting a -1.5% annual return over that time.

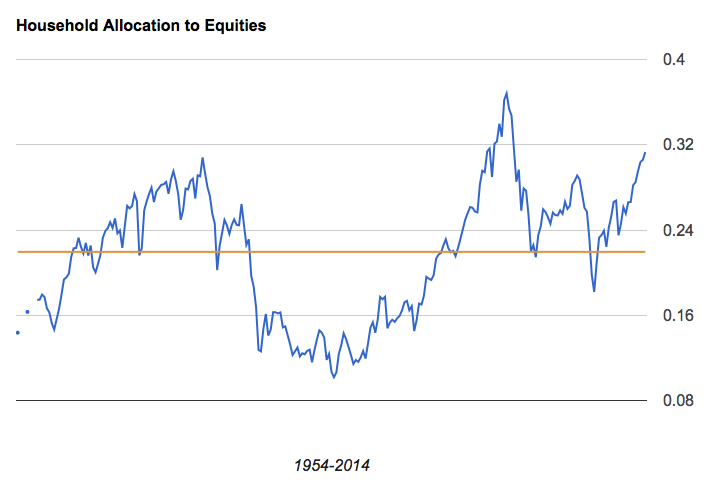

The sentiment measure, household allocation to stocks, is also now higher than it has ever been outside the peak of the internet bubble (though the 1968 occurrence comes close):

It’s even more highly negatively correlated to future returns and now forecasts a 2.4% annual return over the coming decade. The average of the two comes out to about 1.7% and amounts to one of the worst prospective returns in the history of the data. The risk-free rate, on the 10-year treasury, is almost a full percent higher.

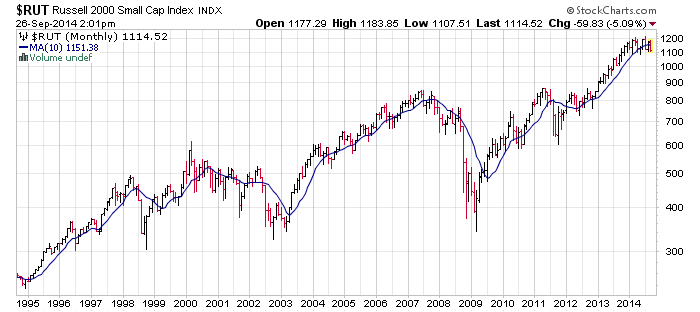

So right now I’m watching the overall trend like a hawk. The S&P 500 and Nasdaq are still well above their 10-month moving averages. However, the Russell 2000 is now more than 1% below its 10-month moving average and the NYSE Composite flirting with its own.

Looking at individual sectors, those that are most in danger of losing their long-term MAs include consumer discretionary, industrials, retail and energy, perhaps the most cyclical sectors of the ten or so I follow. Consumer staples and healthcare, widely considered the most defensive sectors, remain the two strongest. It may be too early to read anything into this but it also may have implications for what’s currently going on in the land of profit margins and the economy.

Ultimately, the uptrend remains in place. However, there are signs that it could be at risk over the next couple of months. With both our fundamental and sentiment measures showing near-record extremes there’s real reason to worry about what the next down cycle will look like. Stay tuned.