Yesterday I found myself reading GMO’s latest quarterly letter and thinking, ‘wow, I’m fairly bearish but Jeremy Grantham just sounds like a grumpy old man!’ Until I came upon this passage:

…you may think that I am particularly pessimistic. It is not true: It is all of you who are optimistic! Not only does our species have a strong predisposition to be optimistic (or bullish) – it is probably a useful survival characteristic – but we are particularly good at listening to agreeable data and avoiding unpleasant data that does not jibe with our beliefs or philosophies. Facts, whether backed by 97% of scientists as is the case with man-made climate change, or 99.9% as is the case with evolution, do not count for nearly as much as we used to believe. For that matter, we do a terrible job of planning for the long term, particularly in postponing gratification, and we are wickedly bad at dealing with the implications of compound math. All of this makes it easy for us to forget about the previously painful market busts; facilitates our pushing stocks and markets on occasion to levels that make no mathematical sense; and allows us, regrettably, to ignore the logic of finite resources and a deteriorating climate until the consequences are pushed up our short-term noses.

It immediately made me think of one of my favorite songs from The Who:

The shares crash, hopes are dashed.

People forget,

Forget they’re hiding,

Behind an Eminence Front,

Eminence Front – it’s a put on.

We are only a few years removed from one of the worst financial crashes in our history and investors have already put it out of their minds. Most importantly they have forgotten perhaps the greatest lesson of that time: overpay for a security and you are essentially taking much greater risk with the prospect of much reduced reward.

GMO's updated 7-year forecasts: pic.twitter.com/Mbmzmoj0sO

— Jesse Felder (@jessefelder) July 16, 2015

Right now, stocks as a whole present very little in the way of potential reward. According to Grantham’s firm, investors should probably expect to lose money over the coming seven years in real terms (after inflation). Other measures (explained below), very highly correlated to future 10-year returns for stocks, suggest investors are likely to earn very little or no compensation at all over the coming decade for the risk they are assuming in owning stocks.

http://twitter.com/jessefelder/status/587737412756844544/photo/1

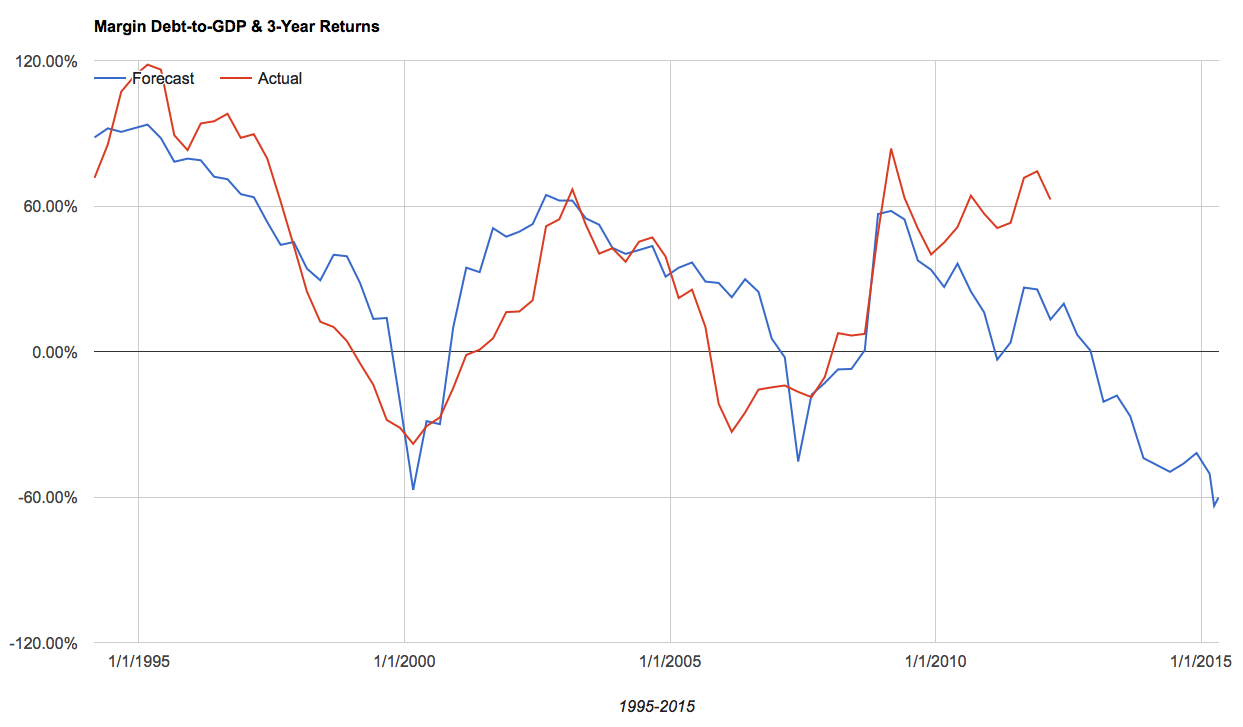

In trying to quantify that risk, Grantham’s firm suggests that investors are now risking about a 40% drawdown in order to earn less than the risk-free rate of return. I have also demonstrated recently that margin debt in relation to GDP has been highly correlated to future 3-year returns in stocks for some time now. The message we can glean from record high margin debt levels is that a 60% decline over the next three years is a real possibility. Know that I’m not predicting this outcome; I’m just sharing what the statistics say is a likely outcome based on this one measure.

This horrible risk/reward equation is simply a function of extremely high valuations. As Warren Buffett likes to say, “the price you pay determines your rate of return.” Pay a high price and get a low return and vice versa. Additionally, if you can manage to buy something cheap enough to build in a “margin of safety,” your downside is limited. However, when you pay a high price you leave yourself open to a large potential downside.

This horrible risk/reward equation is simply a function of extremely high valuations. As Warren Buffett likes to say, “the price you pay determines your rate of return.” Pay a high price and get a low return and vice versa. Additionally, if you can manage to buy something cheap enough to build in a “margin of safety,” your downside is limited. However, when you pay a high price you leave yourself open to a large potential downside.

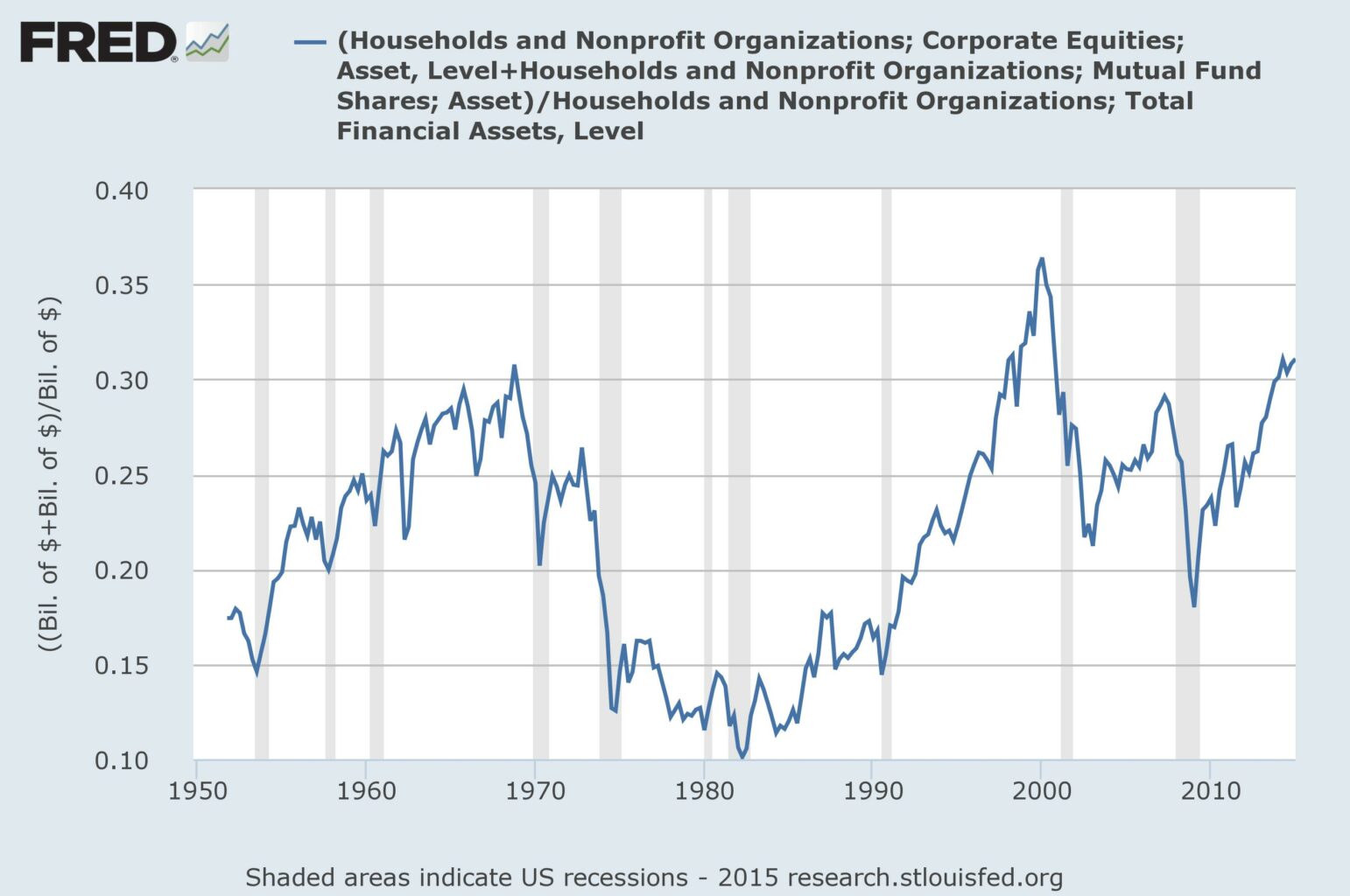

Speaking of Buffett, his valuation yardstick (Market Cap-to-GNP) shows stocks are currently valued just as high as they were back in November 1999, just a few months shy of the very top of the dotcom bubble. Investors should look at this chart and remember what the risk/reward equation back then meant for the coming decade. For those that don’t remember, it meant a couple of massive drawdowns on your way to earning very close to no return at all. (Specifically, this measure now forecasts a -1% return per year over the coming decade.)

Instead, investors today choose to hide behind an “eminence front.” They ignore these facts simply because they are unpleasant to think about. Despite the horrible risk/reward prospects of owning equities today, they have now put nearly as much money to work in the market as they did back in 1999. (This measure is even more highly correlated to future 10-year returns. It now forecasts about a 2.5% return per year over the coming decade.)

Instead, investors today choose to hide behind an “eminence front.” They ignore these facts simply because they are unpleasant to think about. Despite the horrible risk/reward prospects of owning equities today, they have now put nearly as much money to work in the market as they did back in 1999. (This measure is even more highly correlated to future 10-year returns. It now forecasts about a 2.5% return per year over the coming decade.)

It’s truly an astounding phenomenon that investors, after experiencing the very painful consequences of buying high – not just once but twice over the past 15 years, can once again be so enamored with paying such high prices yet again. Amazingly, they are as eager as ever to take on incredible risk with very little possibility of reward. It proves that “rational expectations” are merely the imaginings of academics and have no place in real world money management. It also validates Grantham’s view that it’s not him who is pessimistic; it’s investors who are too optimistic.

It’s truly an astounding phenomenon that investors, after experiencing the very painful consequences of buying high – not just once but twice over the past 15 years, can once again be so enamored with paying such high prices yet again. Amazingly, they are as eager as ever to take on incredible risk with very little possibility of reward. It proves that “rational expectations” are merely the imaginings of academics and have no place in real world money management. It also validates Grantham’s view that it’s not him who is pessimistic; it’s investors who are too optimistic.