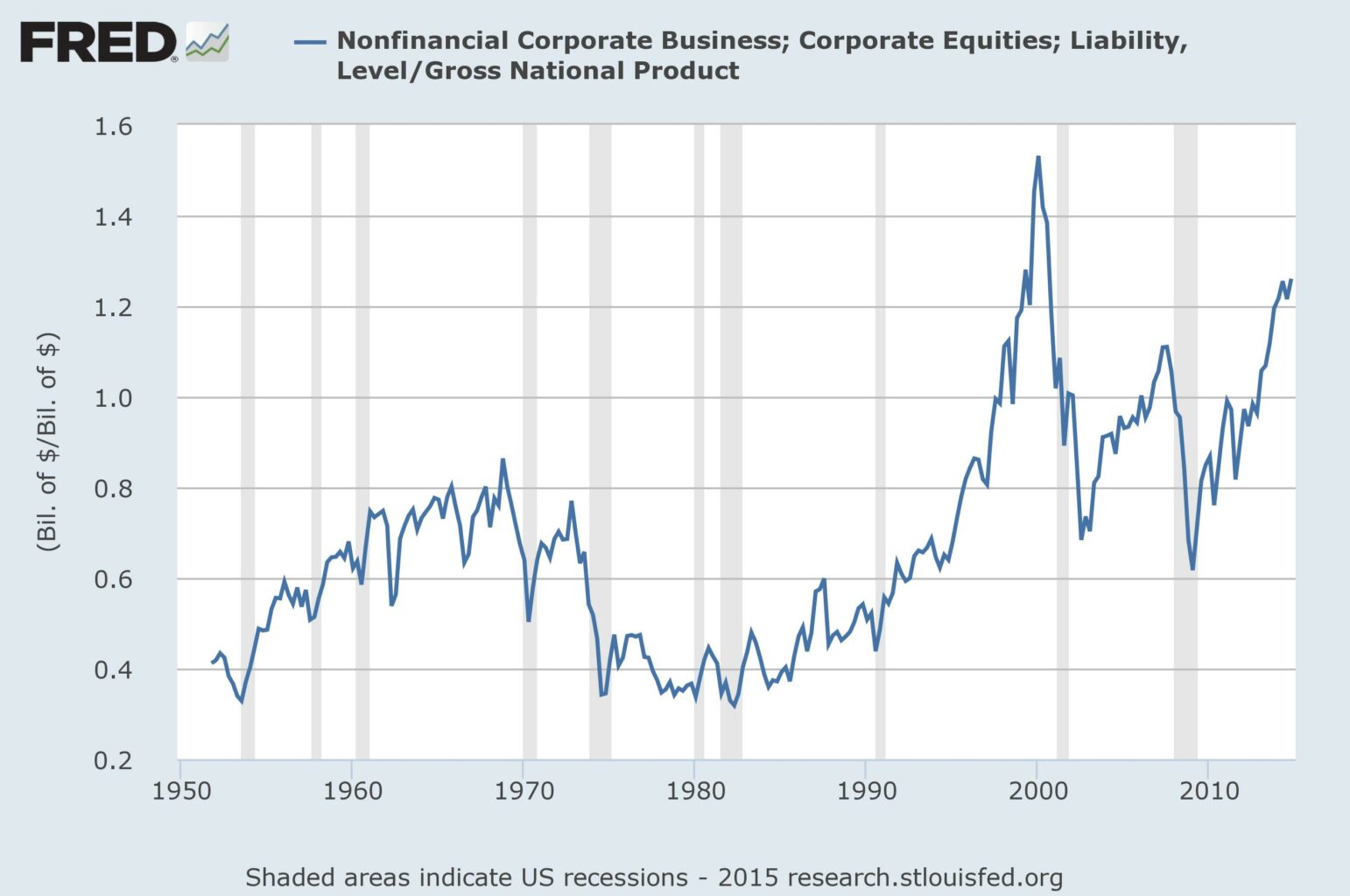

A lot of people have tried to justify today’s extremely high stock market valuations by comparing price-to-earnings ratios to interest rates. Much has been written about why this can be such a problematic way to view equities (see this and this). But here’s one very simple reason why this is potentially a disastrous mistake today: Extremely low interest rates have inflated the earnings side of the price-to-earnings ratio making valuations, at least by this measure, appear far cheaper than they would otherwise. And comparing these inflated earnings-based valuation measures to ultra-low interest rates only compounds the problem.

Carl Icahn recently told Fox Business: “You can borrow money so cheaply and you look at earnings. These earnings are sort of false earnings. They’re based on very low interest rates.” I believe what he’s referring to is the explosion in profit margins which have historically been highly correlated to interest rates. From the chart below it’s plain to see how low interest rates make for higher profit margins and vice versa. Falling interest rates have been a fantastic tailwind for profit margins for decades now. Most recently, ultra-low interest rates have led to record-high profit margins:

Think these high profit margins are sustainable? As Warren Buffett wrote back at the height of the dot-com bubble, “In my opinion, you have to be wildly optimistic to believe that corporate profits as a percent of GDP can, for any sustained period, hold much above 6%.” Today they are roughly twice that level. Paul Tudor Jones recently had this to say about the boom in profit margins: “Right now we might be in the grips of one of the most disastrous [manias] certainly in my career.”

Using price-to-earnings ratios to value the stock market today assumes this profit margin mania will go on forever. Yet, from the chart above it appears that the incredible boom in corporate profit margins may be coming to an end even without a major uptick in interest rates. Still, if rates continue their upward trajectory of the past couple of months it will likely mark the final nail in the coffin for the credit supercycle that has been the major driving force behind this boom (see this). This also means that valuations as measured by price-to-earnings ratios could soar as profit margins revert revealing just how expensive stocks, in fact, have now become.

For this reason, investors are currently being deceived by low interest rates, which suppress price-to-earnings ratios, into believing stocks are cheap especially relative to low interest rates! Once this illusion vanishes, however, they are likely to be very disappointed. This is the thinking behind this sort of statement Icahn made recently: “The interest rate bubble is I think holding [the stock market] up.” Julian Robertson recently attempted to quantify just how dangerous this low interest rate illusion is for the stock market by saying “I don’t think it’s at all ridiculous to think an ’08-size [decline is coming].”

Ultimately, comparing price-to-earnings ratios, which have been corrupted by ultra-low interest rates, to low interest rates themselves amounts to double counting, at the very least. At worst, it’s simply rationalizing an indicator that is not very helpful to begin with in terms of forecasting future returns, which, at the end of the day, is really what investors should care about (see this). So continue to rationalize your exposure to equities however you please. Just know that many of the greatest investors of all time are now taking the other side of that trade.