Periods of low volatility are to investors what a sweet lullaby sung by whispering nanny is to an overtired baby. It relaxes them, gets them to put their worries aside and believe that everything is going to be okay. Great for babies. Not so great for investors.

Because Mr. Market is a sadistic nanny, usually lulling investors into a sense of calm and security right at the worst time.

The few years that led up to the financial crisis were the last great period of low volatility investors witnessed. Clearly, the overwhelming sense of calm in the market (lack of fear), even through the first half of 2007, was unrealistic. You may remember that all of the gains earned during those years were quickly given back and then some during the financial crisis.

But investors were simply doing what they do best: projecting the results of the recent past way out into the future. They were lulled into believing that volatility was no longer cyclical and that the goldilocks economy meant that it was smooth sailing as far as the eye could see.

Alas, we learned shortly thereafter that volatility AND the economy AND the credit markets were, in fact, still subject to cycles.

“Ignoring cycles and extrapolating trends is one of the most dangerous things an investor can do.” -Howard Marks

I bring this up today because volatility has once again witnessed a period of sustained depression and investors have once again been lulled into a sense of extreme complacency (if that’s even a thing).

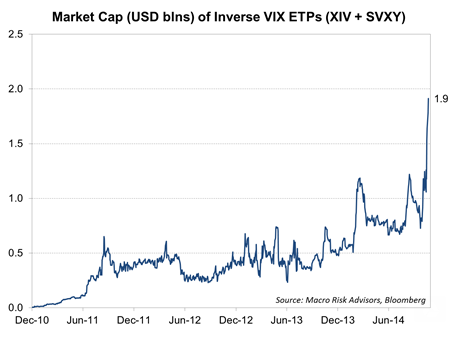

ETFs that track the inverse performance of the VIX have become hugely popular this year. They have now attracted nearly $2 billion in assets, $800 million of that coming just in the month of September. In effect, these are bets that the current period of low volatility will last for the foreseeable future – that’s the only way they will make any money.

Chart via FT.com

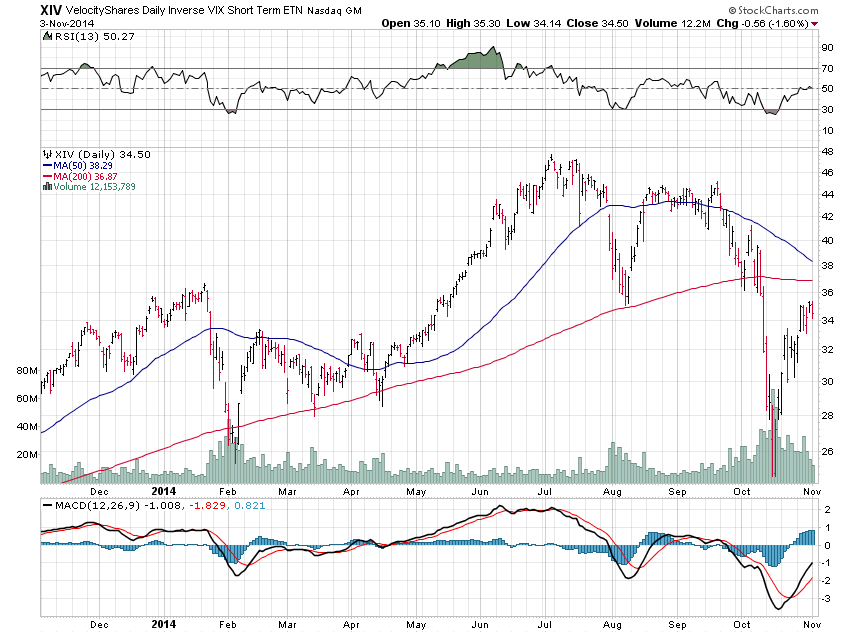

The problem is that the VIX currently stands at about 15. It’s lowest point in the past few decades is around 10. From the beginning of the year to early July when the VIX neared that 10-ish level these ETFs saw about a 35% gain (on about a 35% decline in the underlying index). Nice! Right?

Wrong. During the brief, not-even-10% correction we witnessed last month these ETFs declined nearly 50%!! Imagine what would happen if we actually saw a 20% decline… or more. These funds would be obliterated.

I was recently listening to Tony Robbins on the Tim Ferris podcast and he shared an insight about one thing the world’s greatest investors have in common: they look for fantastic risk/reward setups. They look to risk a penny to make 25 cents. To me this looks just the opposite. It’s like risking 50 cents to make pennies. Good luck with that.

Further reading:

“Now that everyone’s a volatility seller…” – FT Alphaville

“Record short VIX notes sounding alarm to Deutsche Bank” – Bloomberg