Near major turning points in the stock market there is always the fascinating dichotomy of smart money doing one thing and dumb money doing the exact opposite. And by smart money I’m not talking about analysts or brokers or newsletter writers, hardly; I’m talking about corporate insiders. As for the dumb money, I’m talking about Joe Retail trader, your average Wall Street sucker. Without fail the smart money is buying at market bottoms while dumb money is selling and vice versa.

To take off on a brief tangent, for those of you offended by the term “dumb money” know that, in the words of Warren Buffett “when ‘dumb money’ acknowledges is limitations, it ceases to be dumb.” The trouble is that most dumb money doesn’t ever acknowledge the fact that market timing is outside of its abilities. It continues to think it’s smart and buy high and sell low and regard itself as merely unlucky. End of tangent.

Investors haven't been this bullish since 1987 http://t.co/hySjaagwIz pic.twitter.com/yr6ZlFZ5iu

— Jesse Felder (@jessefelder) March 13, 2014

Recent sentiment surveys show that investors haven’t been this net bullish in a very long time. This is valuable to us as a contrarian indicator but these are still just surveys. They reveal what people are saying they’re doing with their money. Looking at what investors are actually doing with their money the picture becomes downright scary.

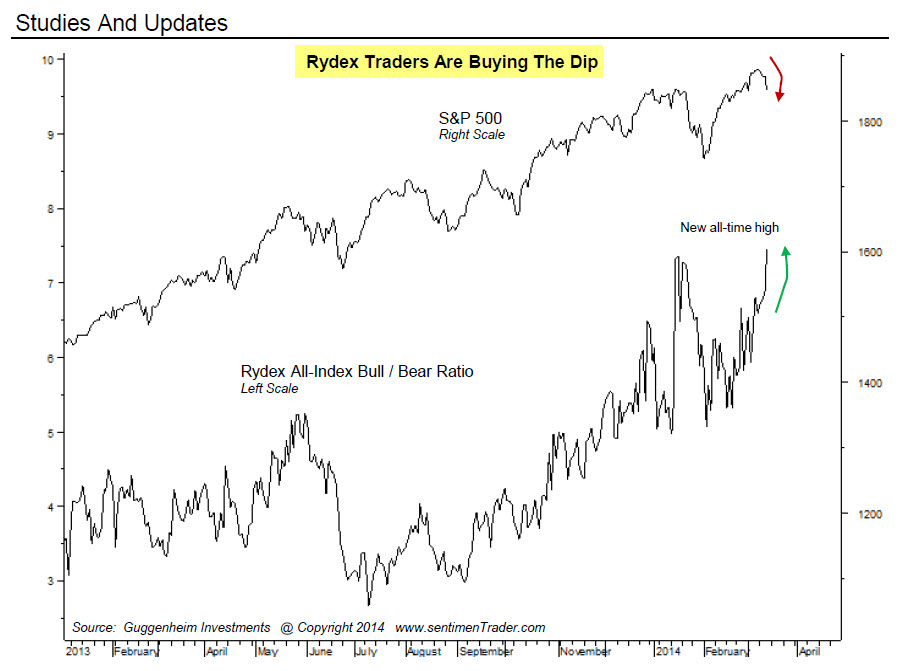

Right now we are witnessing the most extreme example of this dichotomy between smart and dumb money that has ever been recorded. Rydex traders now have nearly 8 times a much money in bullish funds as bearish ones. This is an all-time high:

via SentimenTrader

via SentimenTrader

At the same time, “in-the-know insiders,” corporate officers and directors, have never been more bearish on their own shares. Marketwatch reports:

[blockquote2]Corporate officers and directors in recent weeks have sold an average of six shares of their company’s stock for every one that they bought. That is more than double the average adjusted ratio since 1990, which is when Seyhun’s data begin…. The current message of the insider data “is as pessimistic as I’ve ever seen over the last 25 years,” he says. What makes this development so ominous, he adds, is that, while no indicator is perfect, his research has shown that “the adjusted insider ratio does a better job predicting year-ahead returns than almost all of the better-known indicators that are popular on Wall Street.” There have been two prior occasions when the adjusted insider ratio got almost as bearish as it is today — early 2007 and early 2011. The first came a half a year before the beginning of the worst bear market since the 1930s. While the market didn’t fall as much following the second of these two instances, the May-October decline in 2011 did satisfy — based on intraday levels of the S&P 500 index — the semiofficial definition of a bear market as a 20% drop.[/blockquote2]

When the smart money talks, I listen. And if there’s any dumb money out there reading this I hope this helps you ‘cease to be dumb.’