“I do worry a little bit that we’re beginning to hear things that are reminiscent of the 1999-2000 period—the number of hits, the number of eyeballs. I think if we hold to the old tried-and-true—how many dollars are coming in—then we might be better served. But people are extrapolating, in some way, in a manner similar to the way they did in 1999-2000.” –Art Cashin

When I first read this it immediately reminded me of a study the Fed did on asset bubbles. It determined that bubbles are formed when investors, “extrapolate recent price action [or economic action] far into the future.” And I wouldn’t be surprised if Art was thinking of this when he used the term “extrapolating” in the quote above.

Over the past couple of weeks since he said it, I’ve noticed more than just a few facts that validate Art’s idea that the current stock market environment is eerily reminiscent of the 1999-2000 dot-com bubble. Here are three of them:

1) A prominent group of “sexy” companies has been rewarded/plagued with astronomical valuations. Last week I wrote a brief post about these momentum stocks and how investors ought to watch them for signs of broader market weakness because they typically lead in both directions. But let’s take a look at their current valuations.

Netflix trades at 270 times its trailing earnings; Facebook at 227x; LinkedIn at 850x; Pandora is N/A due to the fact that they have only reported losses (100x projected earnings for next year); Zillow is also N/A for the same reason (147x next year’s earnings); Tesla also has no earnings (94x next year); Yelp! is in the same boat (323x next year); and Priceline.com trades at a relatively cheap 35x.

Now I’m not saying any of these companies are the next Pets.com or even really making any kind of valuation call on any one of them but I don’t think we’ve seen these kinds of multiples since that former company was flying high on investor euphoria. But don’t take my word for it, the CEOs of Netflix and Tesla have recently lamented that their stock prices are way too high. Clearly, they remember what happened to companies that became the target of investor enthusiasm in the bubble years and don’t want any part of it.

2) Investors have become undeniably euphoric. So far this year investors have poured $277 billion in to stock funds, the most since 2000. This is another terrific example of how investors love to buy high and sell low. And while individual investors go gaga for stocks, Warren Buffett, just like he did in 2000, is sitting on a pile of cash practicing his famous maxim, ‘be fearful when others are greedy.’

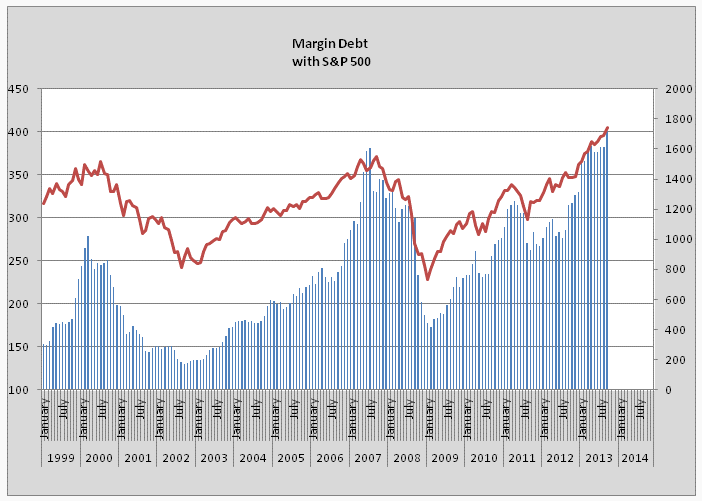

Not only are investors putting cash to work in stocks at record highs in record amounts, they are going into debt to do so. Margin debt levels have recently hit levels only seen at major market peaks, including the 2000 stock market top.

3) Technically (chartwise), stocks’ run from 2009 to 2013 is eerily reminiscent of the run from 1995 to 2000. The chart below comes from Todd Harrison:

What’s more:

of the 1,019 new closing highs on the S&P 500 since 1928, 33 have taken place in 2013 alone (and the most since 1999), says @hsilverb #WSJ

— Jason Zweig (@jasonzweigwsj) October 29, 2013

Happy Halloween!