I’ve been writing for about year now about the Fed’s “confidence game” and its risk to the financial markets. When I first floated the idea I wasn’t too worried about the risks at the time. However, it seems the end game is quickly nearing and so it may now pay to take some risk off. Here’s why:

I’ve been writing for about year now about the Fed’s “confidence game” and its risk to the financial markets. When I first floated the idea I wasn’t too worried about the risks at the time. However, it seems the end game is quickly nearing and so it may now pay to take some risk off. Here’s why:

1) “QUANTITATIVE EASING” JUST ISN’T WORKING

Despite nearly a trillion dollars of money printing over the past year the economy continues to merely limp along. In the words of Martin Feldstein:

The FOMC’s projections in recent years have been repeatedly too optimistic. It looks as though they are repeating the mistake again. At the end of its recent FOMC meeting the Fed released a summary of the economic projections of the FOMC members – the governors of the Fed and presidents of the 12 regional Federal Reserve banks. The central tendency of these projections foresees real gross domestic product growth of 2.0-2.3 per cent for the 12 months starting with the fourth quarter of 2012. That would be higher than the US economy has achieved in any of the past three years. For the first half of 2013 the official annualised GDP growth number is now only 1.8 per cent, and more than one-third of that growth was just inventory accumulation. Private estimates for GDP growth in the current third quarter are at about the same level.

The economy is just not as robust as anyone would like and there are few signs that all this money printing is making a major positive impact.

In his latest press conference Ben Bernanke also expressed his disappointment on the employment front. The headline unemployment rate is 7.3% but it is instructive to look at the percent of the population participating in the workforce. That number has dropped from 51% to 49% over the past six years and the trend is a big headwind to the economy. It may be that people simply give up looking for work. It may also be that the demographic trends in our country are such that we simply have more people retiring than entering the workforce. Either way, QE clearly hasn’t done anything to improve the situation.

2) THE MEDIA AND THE PUBLIC ARE BEGINNING TO LOOK BEHIND THE CURTAIN

Take a look at this new trend in media headlines covering the Fed:

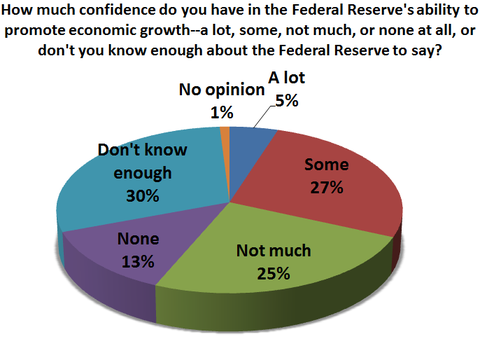

After its decision not to taper QE sentiment toward the FED is clearly turning against it. Even the majority of Americans now believe that QE is a sham:

Notice the actual language in the poll question: “How much confidence do you have in the Federal Reserve….” 38% of respondents answered “none” or “not much” outweighing the 32% said “a lot” or “some.”

This is likely due to the fact that QE’s been most effective in boosting the prices of risk assets which mainly benefits the rich. The majority of the population has seen literally no benefit. Which has led some pundits to suggest that once the general public realizes the cost of all this money printing and that it has only benefitted the wealthiest of the wealthy there may be a serious backlash. (See “Occupy QE” and “Fed accused of covering up soaring inequality“)

3) THE MARKETS ARE NO LONGER TOEING THE FED’S LINE

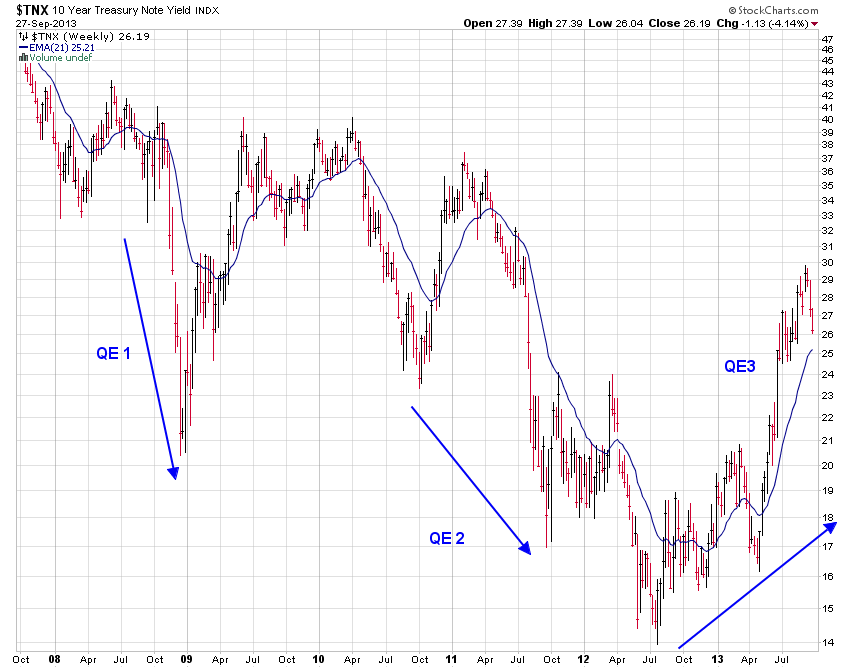

The stock market rallied hard immediately after the no-taper decision but has now given back all of those gains. But the big story is in the bond market. When the Fed started QE1 back in the fall of 2008 rates plunged. They fell once again upon the implementation of QE2 in late 2010. QE3, however, has been met with heavy bond selling and rates have soared even while the Fed has been buying hand over fist:

This should serve as a major warning to investors that the markets are no longer under the Fed’s spell. They may buy a trillion dollars worth of bonds but it’s having literally no impact on long-term interest rates. Make no mistake, the markets are revolting even if the people haven’t yet.

WHAT IT ALL MEANS

Ultimately, I think the the Fed’s quantitative easing measures were necessary and hugely successful during the financial crisis in restoring investors’ faith. After four years of this stimulus, however, it’s slowly lost its power. It’s like a coffee drinker who started with a cup a day and has worked his way up to a couple pots of coffee a day. That first cup in the morning doesn’t do much more than keep him from falling back asleep.

Markets, investors and the economy have built up such a tolerance to QE that $85 billion per month simply doesn’t have any noticeable affect at all – not even on confidence anymore. But the Fed recognizes that without it we’re going to have one hell of a headache. So for now they will continue printing money without tapering because that’s become the de facto neutral.

Still, QE must come to an end at some point. The Fed simply can’t expand its balance sheet by over $1 trillion per year for eternity. This is what precipitated the whole “taper” discussion in the first place. That doesn’t change the fact that it’s going to be a very painful process when it does end. And now it looks like the reality of its impotence, the backlash from the media and the public and, most importantly, the markets are going to force their hand.

Other articles from the past week: